3. Commodities

Supply bottlenecks ensure sustained potential

Dr. David-Michael Lincke, Head of Portfolio Management

In brief

- Despite the slowdown in the global economy, late-cyclical economic momentum meant the commodities markets enjoyed a positive year.

- Although economic risks have continued to rise, the opportunity for moderately positive commodity returns in the coming year remains intact, provided geopolitical challenges such as the ongoing trade conflict between China and the United States can be resolved.

- However, it is important to take a selective approach and advisable to favour commodities facing supply-side bottlenecks or production constraints, as demand-driven commodities and sectors are likely to struggle.

Outlook

Despite a challenging economic environment, the positive returns on commodity markets last year showed that the current upturn in the commodity cycle has not yet reached its end; although falling growth and inflation expectations raise questions about its longevity. But bottlenecks in supply and production point to continued potential in agricultural commodities, especially cereals and raw sugar, as well as in the energy sector. Without an early settlement of the smouldering trade conflict and a brightening of the global economic outlook, base metals may nevertheless continue to struggle. In view of the turnaround in monetary policy and rising risk aversion on the financial markets in the coming year, the greatest upside potential is to be found in precious metals.

Comment

Despite the slowdown in the global economy, the late-cyclical economic momentum meant the commodities markets enjoyed a positive year

The commodity markets delivered a gratifying performance overall in 2019. The rise was led by the cyclical sectors of energy and industrial metals. This largely offset the sharp correction suffered by the commodity markets in the previous year.

Despite the continued slowdown in the global economy and disturbances caused by exogenous factors of a political nature, such as the trade conflict between the United States and China, commodity markets have once again demonstrated their late-cyclical nature. Historically, commodity returns have been particularly robust on average towards the end of an economic expansion cycle.

The strong recovery of the cyclical sectors in particular reinforces our view that we have not yet reached the end of the current commodity cycle.

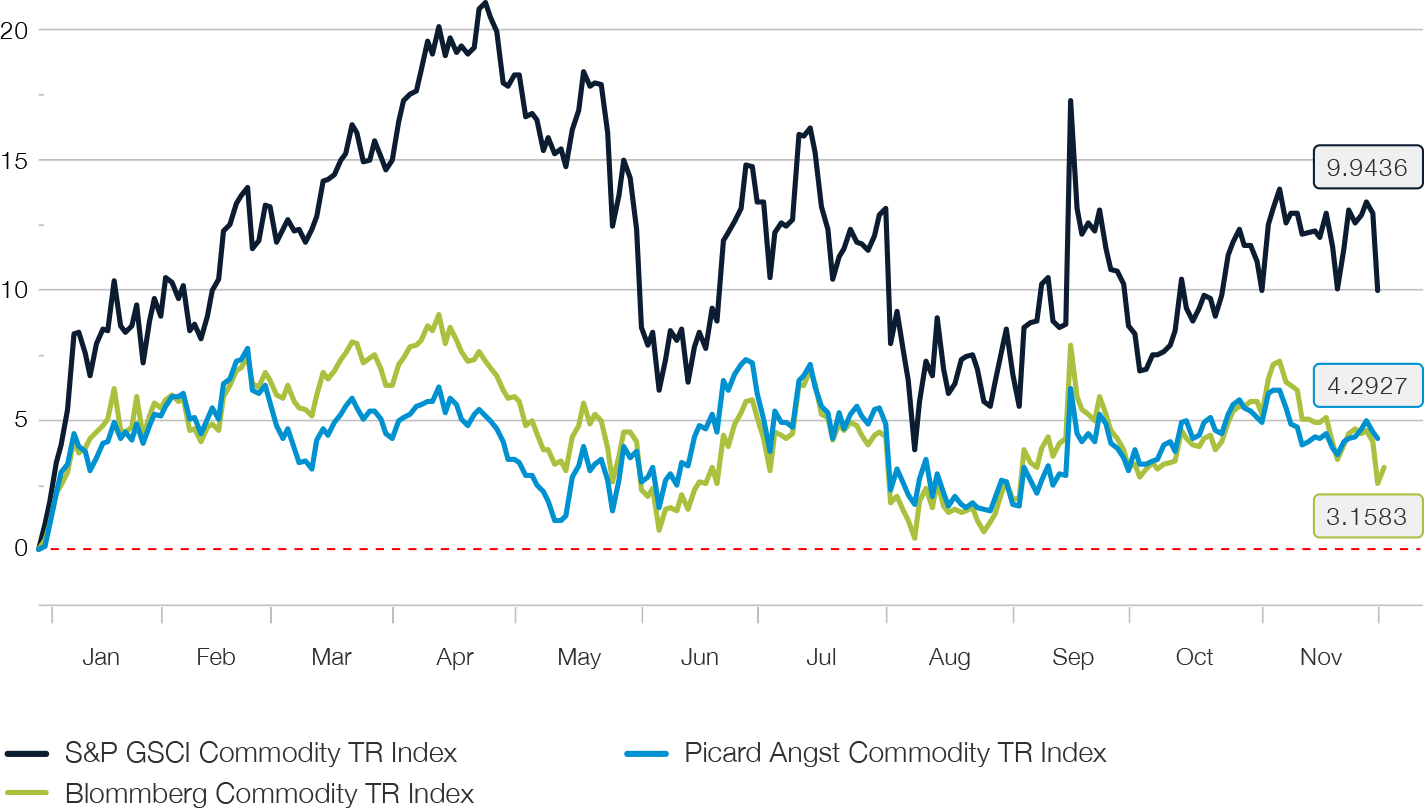

Fig. 23

Picard Angst Commodity TR vs. Benchmark Indices 2019

The leading role played by the energy sector in the recovery of commodity markets favoured strategies with a pronounced cyclical profile. Accordingly, among the broad commodity benchmarks, the extremely energy-heavy S&P GSCI Commodity TR recorded by far the highest gain, even though the correction of the oil price in the second half of the year significantly reduced the degree of outperformance. More balanced benchmarks such as the Bloomberg Commodity TR Index rose more moderately. Despite its comparatively less cyclical sector profile and the weaker development of the agricultural sector, our in-house PACI strategy (investable via our fund product Picard Angst All Commodity Tracker Plus) managed to keep up with the benchmark Bloomberg Commodity TR (see Fig. 23).

Thanks to their concentration on predominantly cyclical sectors, returns were especially high in those strategies that did not take agricultural commodities into account. In this category, our Picard Angst Energy & Metals strategy (which can be invested in via our fund product Picard Angst Energy & Metals) clearly outperformed the benchmark Bloomberg Commodity ex-Ag ex-LS TR.

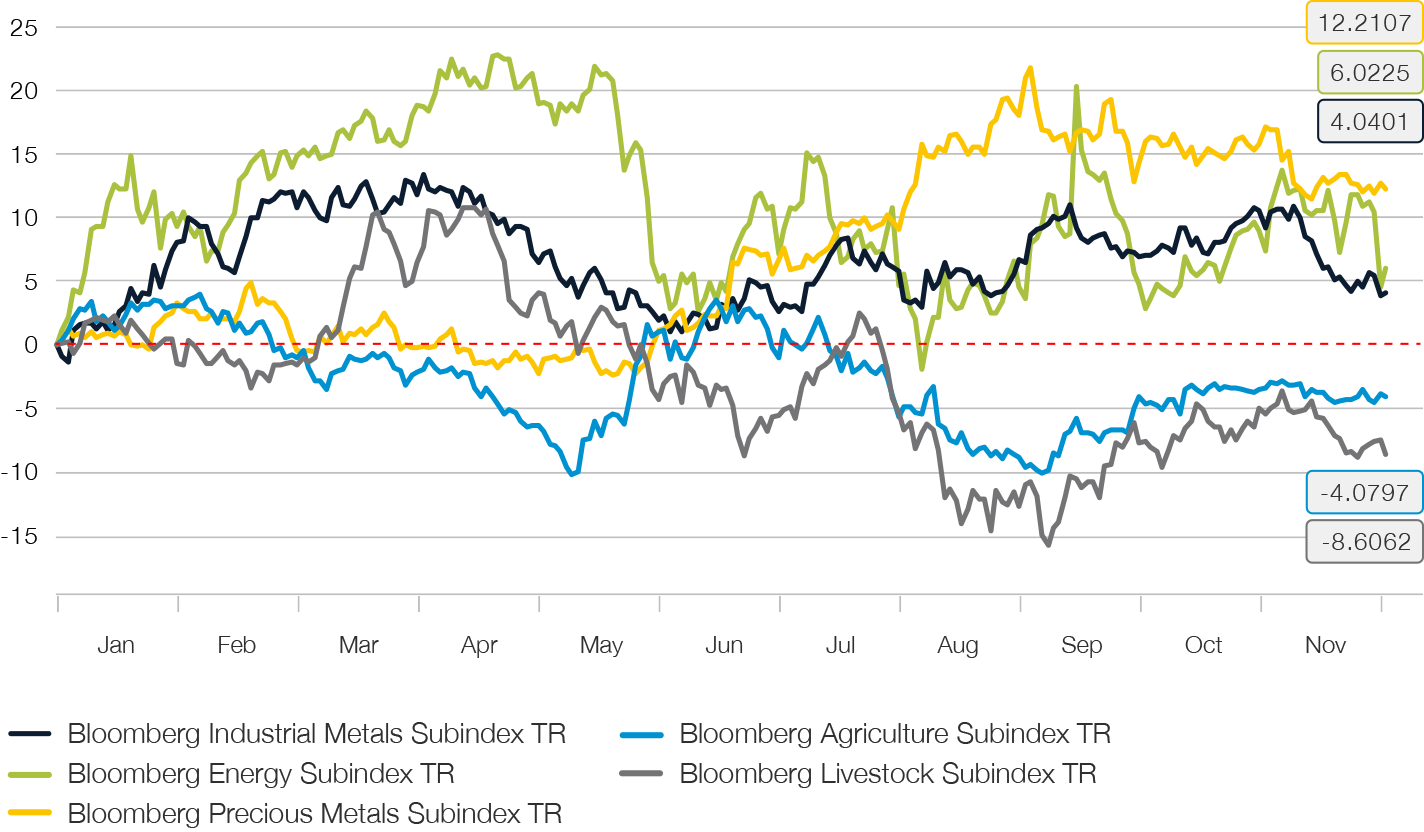

Fig. 24

Development of commodity sectors in 2019

Economic risks continue to grow, but the opportunity for moderately positive commodity returns in the coming year remains intact

In the past, commodity prices experienced the biggest appreciation and outperformed other asset classes when the economic cycle had already peaked, resource shortages were felt and central banks began to hit the brakes. In particular, the pronounced outperformance in the late cyclical expansion phase can be explained by the fact that commodity prices are determined by the supply and demand situation on the spot market – unlike financial equities such as shares, which discount future growth and cash flows. Prices thus rise when the current level of demand exceeds available supply.

Last year, the global economy gradually weakened further, and 2019 is expected to end with global GDP growth of 3% p.a. at best.

Broadly diversified commodity portfolios, for example benchmarks such as the Bloomberg Commodity Index, have required an average growth rate of over 3% in the past to generate positive returns.

For 2020, the International Monetary Fund (IFW) expects a moderate increase in economic momentum to a growth rate of 3.4%. This suggests that the prospect of a positive year 2020 on the commodity markets remains intact.

The gains are likely to be more modest than in the previous year, however, since uncertainty about the economic outlook has also significantly increased. This will be reflected in an increasing dispersion of yield development between sectors and individual commodities. In particular, preference should be given to commodities that are confronted with supply-side bottlenecks or production restrictions, while those driven by demand may struggle. This speaks in favour of positive return prospects, especially for agricultural commodities and also for the oil complex. Selectivity is required with base metals and natural gas, however. If real interest rates remain under pressure and risk aversion returns to the markets, there is a good chance that the upward trend in precious metals will continue.

In addition to economic factors, however, the importance of favourable political conditions must not be overlooked. Despite the reduction of ambitions for a first partial agreement, there is still no end in sight for the trade conflict between the United States and China and the political risks remain high.

In detail, a supporting effect on the raw material markets can be expected in particular from the following factors:

The sharp decline in capital expenditures and investments in new production capacities since the global financial crisis is increasingly becoming a limiting factor when it comes to meeting rising demand.

An increasing proportion of commodities now have declining inventory turnover rates and thus supply deficits. The reduced availability of commodities also has an impact on the maturity structure. For example, the forward curves in the energy sector have inverted significantly and flattened out for individual base metals and agricultural commodities. The rolling return profile for investors has improved as a result.

US monetary policy underwent a radical change of course last year. The factors that have caused the pronounced strength of the dollar in recent years are successively diminishing. A gradual weakening of the dollar is therefore to be expected in 2020, which will have a tailwind effect on the commodity markets.

Despite positive commodities returns, investor exposure to the commodity markets barely broke away from its low level over the past year and remains at the lower end of its historical range. In the past, such constellations have proven themselves to be counter-indicators for investor positioning and have resulted in significantly positive price trends.

Among the risks that could jeopardise a positive scenario for the commodity markets are the following:

Despite intensive negotiations and regular announcements that at least the conclusion of a partial agreement is imminent, the danger of a further escalation of the smouldering trade dispute between the United States and China, as well as the potential for its expansion to the EU, has been by no means put to rest. An unchecked trade war would torpedo any growth recovery of the already troubled global economy and in turn hit demand for raw materials hard.

Economic momentum in China has been much more severely affected by the consequences of the trade conflict than the US economy. A significant further cooling of the Chinese economy would have far-reaching effects on the energy, metal and agricultural markets. China has indeed already introduced a diverse range of fiscal and monetary policy measures to stimulate the economy, but their impact has so far remained modest and there are increasing signs that further room for manoeuvre for economic stimulus programmes is limited in view of the high debt level.

Spot inflation in major economies such as the United States is extremely robust and is close to a ten-year high. Inflation expectations, on the other hand, have fallen significantly worldwide over the past year. Without a reflationary resolution of this divergence, there is little confidence in sustained increases in commodity prices.

In the second half of the year, the interest rate on the underlying capital for commodity investments (collateral yield) fell from over 2% to 1.55% p.a. in the wake of the US Federal Reserve's rate cuts. In the event of a continued economic slowdown, it cannot be ruled out that the collateral return on commodity investments will evaporate again, even on a dollar basis.

Energy

The development of the oil complex in the past year was shaped by the conflict between the efforts of the OPEC cartel and Russia on the producer side to curb an oversupply by cutting production and market participants’ concern about shrinking growth in demand in the wake of the the global economy’s progressive cooling. Accordingly, following a strong recovery at the beginning of the year that lasted until spring, the development of the oil price in the second half of the year was volatile and lacked any sustained trend. Against this backdrop, even a large-scale attack on critical production infrastructure in Saudi Arabia in September, which temporarily switched off 5% of global production, only caused a brief rise in oil prices.

For the coming year, however, we see good prospects that the price of Brent crude oil will approach the USD 70 per barrel mark again. This is supported in particular by the following arguments:

A moderate recovery in global economic growth compared with 2019 should support demand growth for crude oil.

We expect OPEC and Russia to maintain, if not tighten, their production cuts at least until the end of 2020, not least to support the IPO of Saudi Aramco. Ongoing US sanctions against Iran and Venezuela will do the rest when it comes to keeping global supply growth under control.

In the United States, there are increasing signs of a slowdown in the shale oil boom. Exploration activity (measured by the ‘rig count’) fell by a quarter over the past year. This reflects the difficulties faced by the development companies in operating profitably at WTI prices below USD 60 per barrel. The credit and equity markets signal that investors in this sector are increasingly insisting on more discipline and for profitability to be given priority over growth.

The entry into force of the new regulations of the International Maritime Organization (IMO) for more environmentally friendly fuels should substantially increase the demand for oil from the shipping sector by up to one million barrels per day. A slight recovery in world trade should further strengthen demand for distillates.

In combination, these factors should take the supply/demand balance back into deficit in the first half of 2020. In addition to a return of prices to the upper end of the trading range of recent years, investors can also expect to benefit from further increases in rolling yields in the course of such a development.

Industrial metals

The prices of most base metals came under pressure last year. Weaker growth and, in particular, the deterioration in China's economic relations with the rest of the world as a result of the trade conflict have severely dampened investor sentiment and reduced demand.

Nevertheless, many base metals have seen a gradual reduction in inventories on the futures exchanges over the past year, which in other circumstances would not only have resulted in flatter forward curves but would also have had a substantial price-supporting effect. The only positive outlier over the past year is nickel, the price of which at times rose by up to 70%, after Indonesia surprisingly imposed an export ban on crude nickel ore at the beginning of 2020. Nickel also benefits from its potential in the manufacture of batteries for electric vehicles. According to analyst estimates, the amount of nickel required for battery production will increase tenfold over the next eight years.

Assuming an at least moderate recovery of the global economy and a gradual easing of the fronts in the trade war between China and the United States, the prospects for a more pleasing year 2020 in the industrial metals sector are good.

However, it must be taken into account that the prospects for the individual metals will diverge significantly in terms of their supply dynamics. The decisive factor here is whether the supply cycle is dominated by long-term or short-term factors. The medium- and long-term prospects for copper remain positive, as the slump in capital investments since 2013 has brought the supply growth phase to an end and the development of new production capacities is subject to long lead times. In contrast, the aluminium market is likely to face a headwind. The availability of raw materials and the input factor of energy is not limited. However, the supply-side reforms and new environmental requirements in China have cemented higher cost structures, which will prevent prices from falling back to 2016 levels.

The long-term prospects for base metals remain extremely positive. The mining industry is only slowly moving away from a record low in profit margins, which fell to their lowest level since 1998 in 2016. In the past, they proved to be a reliable indicator for the development of the market balance with a delay of about two years. This suggests that the sector will continue to recover in the coming years as supply deficits increase.

Precious metals

In the precious metals sector, the past year was marked by a sustained eruption in the prices of gold, silver and platinum, some of which had been in consolidation for many years. In addition to fundamental factors, technical factors also contributed to this. Investor aversion to the sector had reached historical extremes in the previous year, which once again turned out to be the harbinger of a trend’s turning point.

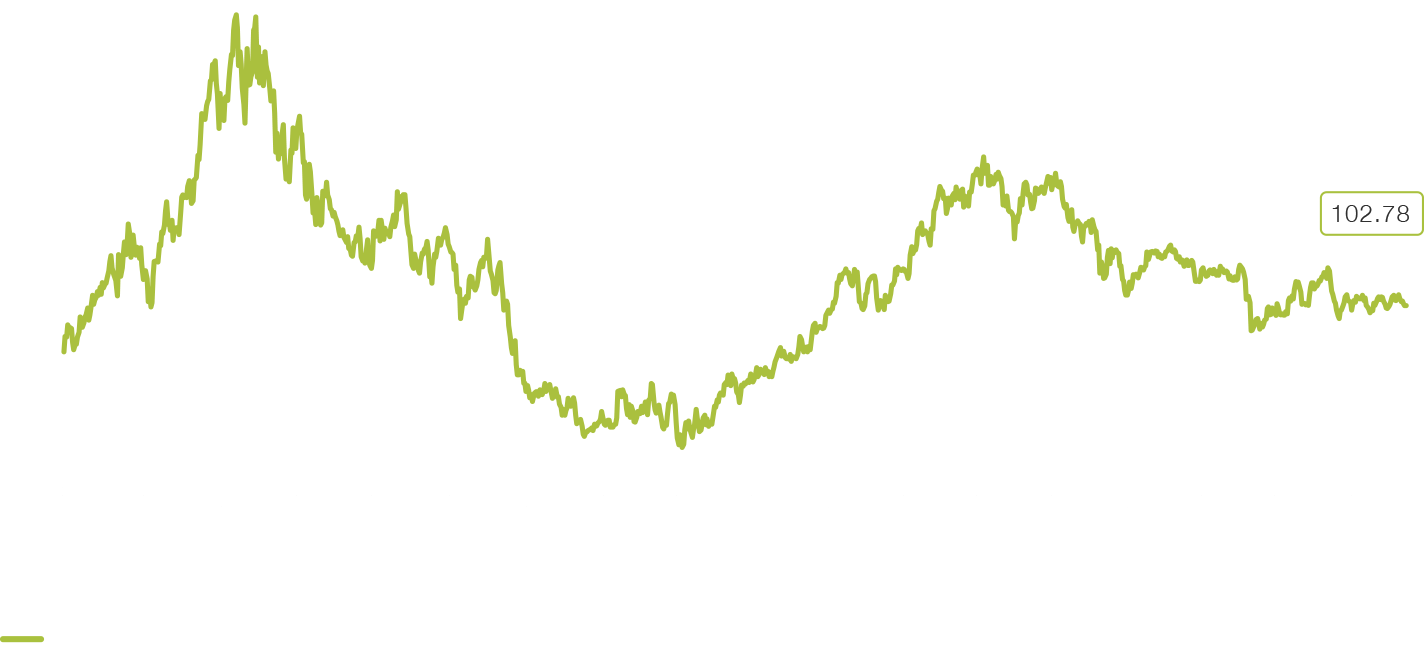

And so, together with prices, the mood of market participants in the precious metals sector has fundamentally changed over the past year. The central banks’ worldwide turnaround away from normalisation of monetary policy towards renewed easing has made a major contribution to this. As a result, long-term real interest rates in the dollar zone, one of the primary determinants of the gold price, have begun a sustained downward trend (see fig. 25:) This helped the gold price to break above USD 1,400 per troy ounce.

Fig. 25

The fate of the gold price remains closely linked to the development of real interest rates

There is a good chance that the upward trend will continue in the coming year. Factors that drove the last long-term rise in the gold price are once again coming to the fore. They include:

Robust physical demand: The demand for physical gold, traditionally dominated by China and India, is beginning to rise again. At present, however, it is primarily central banks that are once again acting as buyers on a large scale to diversify their reserves and have increased their purchases by up to a third in the past year.

Devaluation of the US dollar: Instead of further increases in key interest rates, the US Federal Reserve lowered interest rates three times over the course of the year. At the same time, the room for manoeuvre in the monetary policy of the central banks in Europe, Great Britain and Japan is limited. This should contribute to a gradual depreciation of the dollar in 2020.

Increasing economic and financial market risks: Rising concerns about the outlook for the global economy, geopolitical conflicts and stability risks in view of the historically high leverage of corporate balance sheets should sustainably increase the demand for gold to hedge portfolios.

Risks for a continued rise in precious metal prices emanate in particular from the bond markets. Yields to maturity at the long end have recently stabilised again, but remain caught in a downward trend. However, a sustained upward surge in long-term real interest rates – for instance in the wake of an unexpectedly strong economic recovery – combined with softening geopolitical tensions would call into question a continuation of the bullish gold price.

Agricultural commodities

In addition to base metals, agricultural commodities have felt the effects of the ongoing trade conflict between China and the United States most severely. The result was a noticeable decline in participation in the futures markets for agricultural goods. US soya beans were hit hardest in the price formation, with China reducing a previously used export share of more than 60% to zero. However, the prices of other major US futures contracts on cereals and soft commodities such as cotton also suffered significantly. This development is particularly lamentable for financial investors, who, due to liquidity and market access requirements, are dependent on the contracts of the major US futures exchanges and are generally unable to switch to local markets that are not affected or are benefiting from the situation, for example, for soy beans in South America.

The positive development of supply balances for most cereals, which is reflected in declining inventories, receded into the background in light of this development. This could change in the coming year with a provisional settlement in the trade dispute that substantially increases Chinese imports of US agricultural goods.

In 2019, soft commodity prices, which account for a large proportion of production in emerging markets, suffered primarily from the continued weakness of the EM currencies against the US dollar. This has pushed dollar-denominated prices to historic lows, especially for coffee. The outlook will brighten with the gradual weakening of the US dollar on a trade-weighted basis expected in 2020. Despite new export subsidies introduced by India, there is potential for recovery, especially for the sugar price. This is because the supply and demand balance for raw sugar is moving into an increasing deficit.

Picard Angst All Commodity Tracker Plus

Broadly diversified and systematic investment strategy for commodities in a Swiss fund vessel, which is characterised by a transparent design. Thanks to its advantageous return and risk profile, it is an attractive alternative to the relevant commodity benchmarks.

Source: Bloomberg LP, 04 December 2019

Factsheets and other documents can be found at picardangst.ch/downloads or directly from your contact person.

Picard Angst Energy & Metals

Broadly diversified and systematic investment strategy for commodities. The focus on energy and metals excluding agricultural commodities creates a particularly cyclical profile. Thanks to its transparent design and advantageous return and risk profile, this fund is an attractive alternative to the relevant commodity benchmarks.

Source: Bloomberg LP, 04 December 2019

Factsheets and other documents can be found at picardangst.ch/downloads or directly from your contact person.

Picard Angst Systematic Commodity Alpha

This investment strategy opens up various alternative risk premiums on the commodity markets on the basis of a market-neutral quantitative approach. Irrespective of the development of the broad commodity markets and the traditional asset classes, positive returns are generated in the medium and long term even with moderate volatility.

Source: Bloomberg LP, 04 December 2019

Factsheets and other documents can be found at picardangst.ch/downloads or directly from your contact person.

Share Insight

Important notice

Note that telephone calls on our lines are recorded. By calling us we assume that you agree to your call being recorded. The Swiss Bankers Association’s ‘‘Directives on the Independence of Financial Research do not apply to this presentation. We wish to point out that Picard Angst Ltd. may have interests of its own in the price performance of one or more of the securities described in this document. This document does not constitute an offer or invitation to buy or sell securities. It is intended for information only. All opinions are subject to alteration without prior notification. The opinions expressed here may differ to opinions expressed in other documents published by Picard Angst Ltd. including research publications. Neither the document as a whole nor individual parts of it may be reused or distributed to other parties. Although Picard Angst Ltd. is of the opinion that the information contained in this document is based on reliable sources, Picard Angst Ltd. can accept no liability for the quality, accuracy, current relevance or completeness of this information.

© Picard Angst AG

Regulated by the Swiss Financial Market Supervisory Authority (FINMA).